Let me paint you a picture of a typical Tuesday in the life of a breadwinning kwarentahin.

You wake up, check your phone, and there’s a message from your mom asking if you can pad her grocery budget this month kasi tumaas na naman ang presyo ng bigas. You haven’t even had coffee. Then the kid pops in to remind you that there’s a P1,500 “project fund” due Friday (whatever that means, since back in our day a project meant cardboard and a glue stick). Then your boss pings you about a deliverable.

Welcome to the sandwich generation. You are the filling. Or spread. Or the Star margarine. Nobody asked if you wanted to be it. You just woke up one day in your 40s and there you were, squished between two slices of bread that have become your proverbial rock and a hard place.

I know this one intimately. Years ago, before I had the kid, I watched a huge chunk of my savings disappear into supporting a parent who had renal problems and diabetes and, like most of her generation, no nest egg to speak of. Maintenance meds, hospitalization, eventual funeral. The works. It taught me something uncomfortable that I want to talk about today: in this country, a lot of us were quietly raised to be somebody’s retirement plan. And now we’re raising kids who might be expected to be ours.

Let’s unpack that, shall we?

Children as retirement plan, insurance policy

Here’s the dirty little secret of Filipino “family values.” Utang na loob is weaponized. Either you keep family first or be labeled as the ingrate.

For generations, having kids was not just about love and continuing the bloodline and all that Hallmark stuff. It was a financial strategy. A pretty rational one, actually, back when there was no SSS, no PhilHealth, no mutual funds, and no digital banks offering 6% interest.

Your kids WERE your pension fund. Your kids WERE your hospital insurance. The more kids you had, the more diversified your retirement portfolio (so to speak). Five kids meant five potential income streams to spread the burden of your old age across.

And honestly? It made sense for its time. The problem is that the strategy stuck around long after the math stopped working.

Because here’s what the math actually looks like now. The average SSS pension for a retiree, just before the 2025 reform kicked in, was around P4,923 a month. Let me say that again so it sinks in. Just under five thousand pesos. A month. To live on. The minimum is P2,000 and the maximum is around P24,000, but most retirees cluster near that P5,000 average.

Now tell me, in 2026, what does P5,000 a month buy you? A single trip to the grocery and a couple of maintenance meds and poof, it’s gone. Maintenance meds alone for hypertension and diabetes can eat P3,000 to P5,000 monthly, and that’s before a single hospital visit.

So when Nanay’s pension covers maybe a third of her actual monthly needs, where does the other two thirds come from?

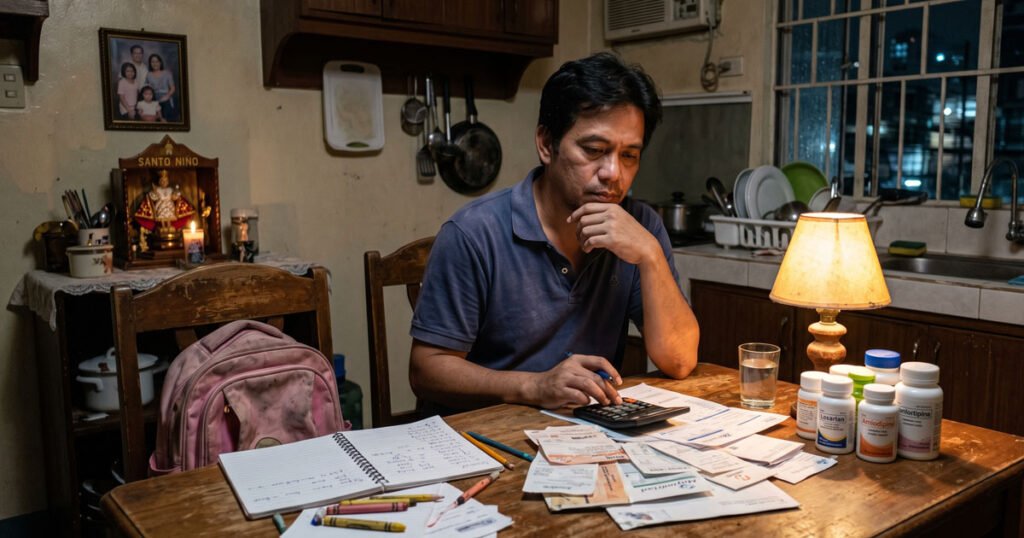

You. The sandwich filling.

That’s the insurance policy nobody told you that you signed. The premium is just “being the responsible anak,” and the payout is your parents’ dignity in old age. There’s nothing wrong with the love behind it. But let’s be honest about the structure, because pretending it’s purely sentimental is how people end up broke at 50 with zero retirement savings of their own.

The actual cost of being the filling

Let me do the kwarentahin math, because numbers don’t lie even when our titas do.

Say you’re a 43-year-old earning a “decent” P60,000 net per month. Solidly middle class. Saktong burgis, even. Here’s a not-at-all-exaggerated month:

- Your own household (rent or amortization, utilities, food, transpo): P32,000

- Supporting Nanay (grocery top-up, maintenance meds, the occasional doctor): P9,000

- The kid (private school tuition spread monthly, baon, uniforms, that mysterious project fund): P11,000

- Your kid’s milk, vitamins, the random fever: P3,000

That’s P55,000 gone before you’ve bought yourself a single thing. You have P5,000 left. Out of that, you’re supposed to build an emergency fund, save for your own retirement, maybe get insurance, and, I don’t know, occasionally feel like a human who is allowed to want things.

Spoiler: most kwarentahins in this exact spot save nothing. Zero. Because there’s nothing left to save. And the cruelest part is that this looks like success from the outside. Decent salary, kid in a good school, parents taken care of. The receipts say “winning at life.” The bank account says “one hospitalization away from disaster.”

The numbers back this up. One study found the average Filipino emergency fund sits around P50,000, and for the sandwich generation that fund gets drained almost immediately the moment a parent has a medical emergency. P50,000 is, what, two nights in a private hospital room? Maybe.

This is the trap. And the trap is generational, which is the whole point of the word “sandwich.” You are paying for the generation above you BECAUSE they followed the old plan of having kids instead of saving. And if you’re not careful, you’ll do the same thing to your own kid.

Enter the trentahin who looked at the math and said “no thanks”

Now here’s where it gets interesting, and where the younger crowd starts making a lot of sense.

The trentahin (and the older Gen Z) have been watching us. They’ve seen what being the filling does to a person. They’ve watched their kuya and ate drain themselves dry supporting lola while raising toddlers. And a growing number of them have quietly concluded: I’m not doing that.

Enter the DINK lifestyle. Dual Income, No Kids. Two salaries, zero dependents, all the disposable income. And its cousins: SINK (Single Income, No Kids) and the wonderfully named DINKWAD, which stands for Dual Income, No Kids, With A Dog. (The dog is the compromise child. The dog does not need tuition. The dog will not be asked to support you in your old age, which is honestly the only flaw in the plan. The cost of kibble and shots though…)

And this isn’t a fringe thing anymore. A Bumble survey found that 59% of single Filipinos are seriously considering a child-free future. Academic researchers studying child-free Filipino millennials found the top reasons were career aspirations, financial considerations, and a desire for personal freedom. Translation: they ran the numbers and the numbers said run.

Can you blame them? The cost of raising a child in this country is now estimated at a minimum of P10,000 a month, which means you’d want a combined household income of at least P60,000 just to do it responsibly. From birth to college, the all-in figure lands somewhere between P3 million and P6 million per kid. Per kid.

A trentahin couple looks at that and thinks: or I could take that P3 to P6 million, invest it, and actually retire on my own terms instead of hoping my future child loves me enough to bankroll my maintenance meds. It’s cold when you say it like that. But it’s also just… math.

The birth rate just confirmed what your barkada already knew

If you thought this was all anecdotal vibes from TikTok, the hard data dropped in 2026 and it’s pretty stark.

The Philippine Statistics Authority’s latest survey found that the total fertility rate has fallen to a record low of 1.7 children per woman in 2025. To give you a sense of the drop, that figure was 4.1 back in 1993. We’ve nearly halved the national baby output in one generation.

And here’s the kicker for anyone reading this from the Calabarzon area like me: our region has the lowest fertility rate in the country at 1.3. Urban areas overall sit at 1.5, rural at 2.0. We’ve dropped below the 2.1 “replacement rate,” which is the number you need just to keep the population from shrinking. We are now, officially, not making enough Filipinos to replace ourselves.

Let that demographic reality marinate for a second, because it has a brutal long-game implication for the sandwich generation. Fewer kids being born today means fewer working-age citizens in 30 years to spread the elder-care burden across. The old “have five kids, divide the burden by five” plan is dead. The trentahin having one kid (or zero) means that one kid, if they exist at all, inherits the WHOLE sandwich solo. No siblings to split lola’s hospital bills with. No group chat where you guilt-trip your brother into paying his share.

So the cycle isn’t just continuing. For the smaller families of the future, it’s actually getting more concentrated and heavier per person. Unless we break it.

So how do you stop being the filling (or at least a thinner filling)?

I’m not going to give you the standard “just budget better” advice because if you’re sandwiched, you already know how to budget. You budget like a hostage negotiator. The issue isn’t discipline. It’s structural. So let’s talk structure.

Be the last sandwich generation in your family. This is the mindset shift that matters most. The goal isn’t to refuse to help your parents (we’re Filipino, that’s not happening and honestly it shouldn’t). The goal is to make sure you don’t pass the sandwich down to your kid by retiring on your own steam. Your own SSS, your own savings, your own investments, your own insurance. So that when you’re 70, your anak gets to keep their P5,000 instead of handing it to you.

Separate the love from the leak. Helping a parent through a genuine crisis is love. Funding a fully able relative’s lifestyle indefinitely is a leak. Years ago I wrote that you should take a quiet survey of who in your life actually gives you a decent return on your emotional and financial investment, and protect numero uno first. I stand by it. Generosity with no boundaries isn’t virtue, it’s just slow-motion self-sabotage.

Use the discounts and programs that already exist. Your senior parents are entitled to senior citizen discounts of 20% on medicine, medical services, and transport. Some LGUs hand out monthly cash aid, free check-ups, or groceries for seniors. PWD benefits exist too. These won’t solve everything, but every peso the government covers is a peso that doesn’t come out of your filling.

Build YOUR fund first, even if it feels selfish. This is the airplane oxygen mask rule. You cannot pour from an empty tumbler. If you sacrifice your entire retirement to support everyone around you, you simply become next decade’s burden. Even P2,000 a month into a low-cost index fund or a digital bank at age 43 is infinitely better than P0 and a prayer that your kid loves you enough.

Have the awkward conversation. Sit your parents and your spouse down. Talk numbers out loud. Who covers what. What the actual gap is. What happens during a hospitalization. Filipino families avoid money talk like it’s bad luck, and that silence is exactly what lets the burden land on one unlucky filling by default.

The unsexy truth

The sandwich generation exists because of a financial literacy gap that skipped a generation, plus a cultural script that turned children into a retirement product. None of that is anyone’s individual fault. Our parents did what their parents did. The plan made sense once.

But you are standing at the exact point where the cycle either repeats or breaks. The younger generations choosing DINK and DINKWAD lives aren’t villains abandoning Filipino values. A lot of them are just the first people in their family to look at the spreadsheet honestly and refuse to sign up to be somebody’s pension fund.

You don’t have to go child-free to learn from them. You just have to make sure that when it’s your turn to be old, you’re nobody’s filling, and your kid gets to keep their sandwich whole.

Nanay deserved better than P5,000 a month. So do you. So does the kid.

Start there.