Once upon a time, when I was teaching at university, my fellow junior faculty and I had that talk about how our careers are panning out. Sadly, at that time, the outlook for us was bleak. Overworked. Underpaid. Financially drowning. We all wanted to explore life outside the academe, which we all eventually did once we overcame utang na loob.

As for why we were there in the first place, most of us went into teaching because we felt obligated to do it. Our mentors urged us to do it, often framing it as a way to give back after they molded us to become the scholars that we were. At that time, they even even demonized BPOs just to get us to pursue the “nobler path.” In hindsight, BPOs would have been the more lucrative choice.

Utang na loob can be a bitch. For a huge chunk of the Filipino middle class, we can pay for it dearly. We often. Unlike conventional debt where there’s an actual figure that can be dealt with, reciprocity of utang na loob often isn’t or can’t be defined. Madalas, walang katapusan.

Let me explain what I mean, because I think a lot of us are quietly going broke over something we were taught to be proud of.

What utang na loob was actually supposed to be

First, let us be fair to the concept. Utang na loob is not the villain here.

Translated loosely as a debt of gratitude, the term was first rendered into English by anthropologist Charles Kaut back in 1961. But the literal meaning is closer to “a debt of one’s inner self.” It lives in the world of kapwa, the shared sense of self that Filipino psychologists put at the center of how we relate to other people.

In its purest form, it is beautiful. Someone helps you in a moment that truly matters, and you carry that warmth forward. You look for ways to return the goodwill. The relationship deepens. Walang masama doon.

The problem is what happens when a relational value gets treated like an actual loan. With interest. Compounding. And a collector who knows exactly which guilt button to press.

Even the academic literature admits the term gets “misunderstood and misused,” to the point that many Filipinos now experience it as burdensome, even toxic. That gap, between what utang na loob is supposed to be and how it actually gets weaponized, is where the hidden tax lives.

Here is where it shows up most.

Tax #1: The eldercare bill your parents pre-assigned to you

Let us start with the big one, because this is the bracket that hits hardest and earliest.

In most Filipino families, the math was decided before you were born. Your parents raised you. Therefore you owe them. Therefore when they grow old, their care becomes your line item.

And here is the part that surprises people: it is not just culture. It is literally in the law. Section 4, Article XV of the 1987 Constitution states that the family has the duty to care for its elderly members. The State will help, but the burden is designed to land on you first.

Now look at how thin the government backstop actually is. The DSWD social pension for indigent senior citizens pays a grand total of ₱1,000 a month. That figure was doubled (from a measly ₱500) under RA 11916, and even then, you only qualify if you are frail, have no income, AND have no family able to support you. In other words, the moment you exist and have a salary, the State quietly steps back and hands the bill to you.

So who is covering the gap? You are. Over 90 percent of Filipinos say they do not have enough money for their own retirement, which means a generation of parents reached their 60s with no nest egg, and the plan was always to lean on the kids.

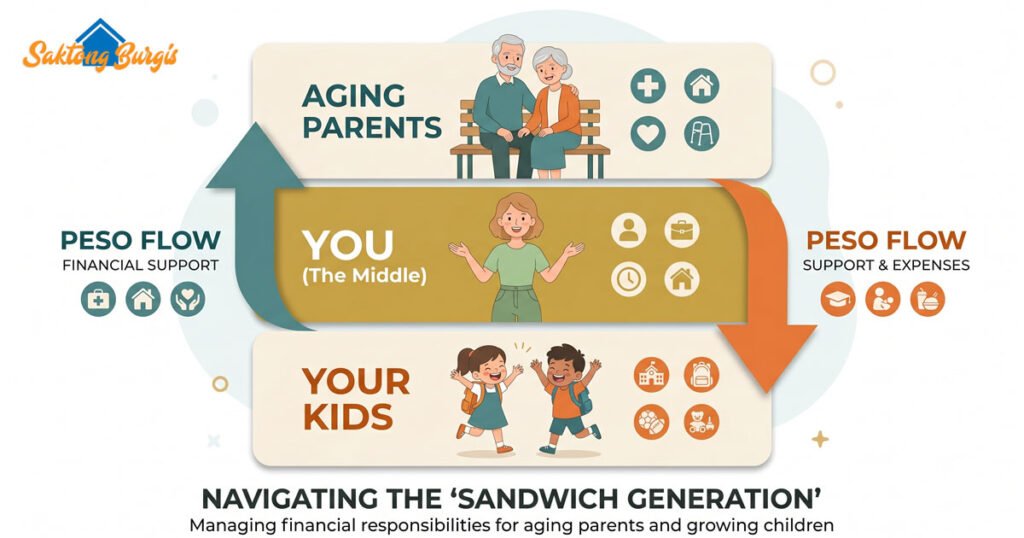

This is the famous sandwich generation. Roughly 34 percent of Filipinos are taking care of a family member, squeezed between aging parents above and their own children below. Picture a 38-year-old earning ₱60,000 in Makati, sending ₱8,000 a month to her parents in the province, paying ₱15,000 in tuition for two kids, and wondering why she cannot save a single peso. She is not bad with money. She is paying a tax nobody warned her about.

And let me say the quiet part out loud, the way I wish someone had said it to me years ago. Helping parents who genuinely have nothing? That is not a tax. That is love, and it is the right thing to do. But there is a difference between helping a mother who worked her whole life and never had a chance to save, and bankrolling a parent who simply expects to be carried because “anak ka namin.” The first is utang na loob. The second is just somebody else’s poor planning, billed to you.

Tax #2: The boss who lords loyalty over you instead of giving a raise

The second tax is sneakier, because it wears a corporate ID and pretends to be loyalty.

You know the type of boss. The one who “took a chance on you” when you were fresh out of school. The one who “gave you your first break.” And then, for the next six years, reminds you of it every time you so much as glance at a competitor’s job posting.

“After everything we did for you, aalis ka na lang?”

That is utang na loob being used as a retention tool. And it is brutally effective, because it converts a normal professional relationship (you provide labor, they provide salary) into a moral debt that has no payoff schedule. You start declining better offers, negotiating, and accept the “we are like a family here” line.

Here is the financial damage in plain numbers. Career strategists generally agree that the fastest way to grow your income early on is to change jobs, where switching can mean a 10 to 20 percent jump versus the 3 to 5 percent annual increase you get for staying loyal. Stay “out of utang na loob” for five years, and you can easily leave hundreds of thousands of pesos on the table. That guilt has a price, and you are the one paying it, kasama ang pamilya mo.

Loyalty is a virtue. But loyalty is supposed to be mutual. If your gratitude only ever flows one direction, and the company would replace you in two weeks without a second thought (they would), then it was never utang na loob. It was leverage. Alamin mo ang difference.

Tax #3: The barkada loan you already know you will never see again

The third tax comes from the side you least expect: your friends.

Picture the scenario. A close friend messages you. Emergency daw. Can you lend ₱20,000? You have it, technically, sitting in the fund you were building for something specific. You also know, deep in your gut, that this is the third “emergency” this year, that the money is not coming back, and that lending it is a genuinely bad financial move.

And yet you say yes. Why? Because saying no feels like a betrayal of the relationship. Because “ang kapal naman kung tatanggihan.” Somewhere along the way, friendship got tangled up with the obligation to bankroll each other’s poor decisions.

The data shows just how baked-in informal lending is to Filipino life. While borrowing overall has been dropping, a BSP survey found that around 10 percent of adults still rely on informal lenders, the barkada, the kapitbahay, the “5-6” guy, instead of formal channels. We lend to each other constantly, often with zero paperwork and even less expectation of repayment.

Part of why this works on us is that we are, collectively, not great with this stuff. In the BSP’s financial literacy assessment, only 2 percent of Filipino adults correctly answered all six basic questions on money. So we are making high-stakes lending decisions, driven by guilt, with very little financial grounding.

Here is the test I now use. A real friend who borrows out of genuine need feels the weight of it and tries to pay you back. A taker leverages the friendship precisely because they know you are too kahiya to say no. The first is someone you help. The second is someone running a tab on your kindness.

How to pay your utang na loob without going bankrupt

So what do we do? Stop helping people and become a heartless tightwad? Hindi naman.

The goal is not to cancel utang na loob. It is to stop letting other people compute the amount for you. Here is how I think about it now.

Give utang na loob a line item. The fastest way to stop bleeding is to make the invisible visible. Decide, in advance, how much you can sustainably give to family each month, say ₱5,000 or ₱8,000, and treat it like rent: fixed, budgeted, non-negotiable in either direction. When the requests come in above that line, you are not refusing your family. You are refusing to skip your own emergency fund. Big difference.

Separate love from leverage. Before you say yes to anything, ask one question: am I returning genuine goodwill, or am I being managed? Goodwill earns help freely. Leverage uses guilt to extract it. Once you can tell them apart, half the “obligations” in your life quietly disappear.

Protect future you first. This is the one nobody wants to hear. If you bankrupt yourself caring for the generation above you, you become the exact same burden to the generation below you. The kindest, most utang-na-loob thing you can do for your own kids is to fund your own retirement so they never have to carry you. Saving for yourself is not selfish. It is breaking the cycle.

“No” is a complete sentence (with Tagalog subtitles). You will not master this overnight. But “Pasensya na, hindi ko kaya ngayon” is allowed. The guilt that follows is not proof you did something wrong. It is just the tax collector realizing the ATM is finally out of service.

Stop the toxicity

Utang na loob, at its best, is one of the most beautiful things about being Filipino. The warmth, the kapwa, the instinct to take care of each other. We should protect that.

But we should also stop letting it quietly drain the people who can least afford it: the middle-class earner who looks rich on paper and is one hospitalization away from disaster, all because they have been paying a tax that nobody ever put in writing.

Compute your own utang na loob tax this month. Saan napupunta talaga ang pera mo, at sino ang nagdedesisyon nun? Ikaw o ang hiya mo?