So you finally have a little extra at the end of the month. Maybe ₱2,000, maybe ₱5,000 on a good month. And every payday you tell yourself you will “invest” it, then it quietly disappears into GrabFood and that sale on Shopee you swore you would skip.

Not investing sooner and diversifying my portfolio remains to be among of my bigger regrets money-wise. It’s tough to outpace inflation if you don’t invest in higher-yielding things.

So, if you have an extra amount you could spare, sound financial thought would say invest and grow it. Spoiler: there is no right amount to get started. You can always start small, start boring, and and start on the safer side.

This is a beginner’s walkthrough of the three investment vehicles most ordinary Filipinos can actually access without a financial advisor on retainer: MP2, UITFs, and REITs.

I am going to be deliberately conservative here, because the internet is already full of people promising you will get rich. I am not one of them. And a quick disclaimer before we go further: We are not financial advisors. Everything in this post is general information, not personalized advice. For anything involving your specific situation, talk to a licensed professional.

First, the essentials

Before you put a single peso into any of these, make sure you have these things dealt with. Walang shortcut.

One, you have an emergency fund. Three to six months of expenses, sitting in a plain savings or digital bank account where you can grab it fast. Investments are not emergency funds. If you have to sell your REIT shares in a panic because your phone died and you need a new one, you have already lost. (Here’s a guide on how to build an emergency fund if you need a starting framework.)

Two, you have killed your high-interest debt. If you are carrying a credit card balance at 3% per month, that is roughly 36% a year. No investment here will reliably beat that. Paying off that card is your best move.

Three, the money you invest is money you will not need for at least five years. All three options below reward patience and punish people who pull out early. If you might need the cash next year, this is not the place for it.

Done? Okay, let us talk options, from safest to spiciest.

MP2: the safe and boring one

Let us start with the one I recommend to almost every beginner: the Modified Pag-IBIG II Savings Program, better known as MP2.

MP2 is a voluntary savings program run by Pag-IBIG, the same government agency that handles your housing loans. It is separate from your regular mandatory Pag-IBIG contributions. You put in money, you leave it for five years, and it earns dividends.

Here is why I like it for beginners:

- Government-backed. Pag-IBIG is a state-run fund, and by law it must return at least 70% of its annual net income to members as dividends. This is about as close to “safe” as investing gets in this country.

- The returns are decent and tax-free. The MP2 dividend rate was 7.05% in 2023, 7.10% in 2024, and a record 7.12% for 2025. Compare that to a regular bank savings account paying you a sad 0.25%. And walang tax na kakaltasin sa dividends mo.

- Low barrier to entry. Minimum is ₱500 per remittance. No maximum (though large lump sums need extra paperwork).

- You can pay via GCash or Maya through Virtual Pag-IBIG. No need to fall in line.

One important caveat I want to be honest about: that 7.12% is declared every year, not locked in for the full five years. Pag-IBIG announces a new rate annually based on how the fund performed. It has hovered around 7% recently, but do not assume it is guaranteed forever.

Here’s a quick example. Say you drop ₱100,000 into MP2 and leave it for five years at roughly 7%. You walk away with about ₱141,000, so around ₱41,000 in earnings, completely tax-free. Or if you are doing the steady ipon route at ₱2,000 a month for five years, that is ₱120,000 of your own money growing to roughly ₱138,000.

Hindi ka yayaman overnight. But it beats inflation (barely), it is predictable, and it builds the habit. For most people reading this, MP2 should be your first stop, not your last.

The catch: pre-terminating early means you forfeit 50% of the dividends you earned, and early withdrawal is only allowed for specific valid reasons (retirement, migration, layoff, OFW repatriation, critical illness, and a few others). So again: only money you can leave alone.

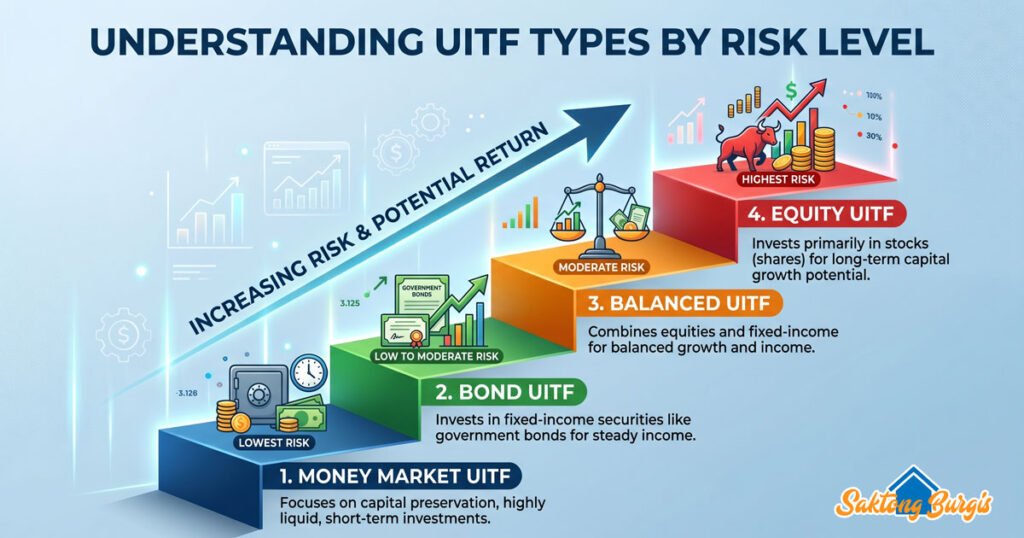

UITFs: letting a pro drive

Next up the risk ladder: Unit Investment Trust Funds, or UITFs.

A UITF is a pooled fund. Your money gets combined with thousands of other investors, and a professional fund manager at a bank invests the whole pot in things like government securities, bonds, or stocks. You buy “units” of the fund, and the value of each unit (the NAVPU) goes up and down with the market.

UITFs are offered by banks with trust licenses and are regulated by the BSP. Here is the part beginners gloss over and should not: a UITF is not a deposit, and it is not insured by PDIC. If the market drops, your units can be worth less than what you put in. Walang guarantee sa principal.

There are four main types of UITFs, roughly from lowest to highest risk:

- Money market funds. Short-term, very low risk, modest returns. A decent parking spot for cash you want slightly more productive than a savings account.

- Bond funds. Invest in government and corporate bonds. Moderate risk, steadier than stocks.

- Balanced funds. A mix of bonds and stocks. Middle of the road.

- Equity funds. Mostly stocks. Highest potential returns, highest chance of seeing red.

You can start small. BDO lets you begin with as little as ₱1,000 through a regular investment plan, while others like RCBC start around ₱5,000. The fund charges a trust fee (usually around 1% a year) and that is mostly it. No big sales commissions like some mutual funds charge.

My conservative take for beginners: if you are going to try a UITF, start with a money market or bond fund, not an equity fund. The equity funds can swing wildly, and a lot of newbies buy high in excitement, panic when it drops, and sell low. Let your stomach get used to seeing the number move before you add risk.

REITs: owning a slice of the building

Now the spiciest of the three for beginners: Real Estate Investment Trusts, or REITs.

Ever walked through a mall in Makati or an office tower in BGC and thought, “Ang laki ng kinikita nito, sana ako ang may-ari”? A REIT lets you own a tiny slice of exactly those kinds of properties without needing millions for a down payment.

REITs are companies that own income-generating real estate (malls, offices, warehouses, even solar farms). They collect rent, then pass most of it to shareholders as dividends. They trade on the Philippine Stock Exchange just like regular stocks, so you buy and sell them through a stockbroker.

The big appeal is the law. Under the REIT Act of 2009 (Republic Act 9856), a Philippine REIT must distribute at least 90% of its distributable income to shareholders every year. That mandatory payout is why REIT dividend yields tend to run higher than ordinary stocks, often in the 6% to 8% range.

Some of the names you will see on the PSE:

- AREIT, the first one listed, backed by Ayala Land. Considered one of the more stable, with a yield on the lower end.

- MREIT (Megaworld), RCR (Robinsons), FILRT (Filinvest), DDMPR, and CREIT (Citicore, the renewable-energy one).

[IMAGE 4 here: A clean illustration of a hand holding a small puzzle piece shaped like a Makati office tower, symbolizing fractional real estate ownership. Alt text: “Investing in Philippine REITs on the Philippine Stock Exchange.” Export as WebP, lazy-load.]

Now the conservative reality check, because REITs get oversold as “passive income na walang risk.” Hindi totoo yan.

- REIT prices fluctuate. It is a stock. The dividend might be steady, but the share price can fall, and if you sell at the wrong time you lose money on the capital side. Some REITs are below their listing price.

- Dividends are taxed. Local individual investors pay a 10% final withholding tax on REIT dividends. So that 6.5% yield is really closer to 5.85% in your pocket. (On ₱100,000, that is about ₱5,850 a year after tax.)

- The office market is wobbly. With work-from-home and the POGO exit, some Metro Manila office buildings are sitting with high vacancy, especially in fringe areas. REITs heavily exposed to those are riskier than ones holding prime Makati or BGC assets.

- Do not chase the highest yield. A suspiciously high yield often means the share price already crashed. Read why before you buy.

If you go this route, my conservative advice: stick to the well-established REITs with strong sponsors, do not bet your whole stash on one, and treat the dividends as the reward for patience, hindi yung araw-araw na panonood sa price.

So which one should you pick?

If you made me line them up for a beginner on a regular salary, this is roughly how I would think about it:

- Just starting, want safety and a habit? MP2. Tax-free, government-backed, predictable. Start here.

- Ready for a bit more, comfortable with small ups and downs? A money market or bond UITF. Let a pro manage it while you learn.

- Want exposure to property and steady dividends, and you can stomach price swings? A small position in an established REIT, with money you will genuinely leave alone for years.

Honestly? There is nothing wrong with putting most of your money in boring old MP2 and only dipping a small amount into a UITF or REIT to learn. That is not being timid. That is being smart while you are still figuring out your own risk tolerance.

Personally, I do not have the appetite or stomach for big risks, so my portfolio is mostly in the safer ones. The goal is not to look like a stock-market genius on Facebook. The goal is to quietly, boringly, end up with more than you started with. Slow ang ipon, pero steady.

What about you? Are you team boring-but-safe MP2, or are you itching to try the market with a UITF or REIT?